Version française/French version: LINK

We modeled the performance of four venture capital investment portfolios. Their outcomes can be unprofitable, neutral, or highly profitable depending on the multiples generated by a limited number of investments. Apart from the most unfavorable scenario, the structure of the other three portfolios is identical: only the multiple of the most profitable investment varies. This demonstrates that the presence of an exceptional or « home run » investment can transform an average portfolio into a highly performing one, ranking in the top quartile of venture capital.

During the gold rush between 1848 and 1855, approximately 300,000 people traveled to California hoping to strike it rich. Today, the United States has a comparable number of business angels whose quest for precious metals has turned into a pursuit of capital gains from selling their stakes in startups.

While the hunt for unicorns —companies valued at over $1 billion— is as arduous as discovering a gold vein, the approach differs significantly from that of the past.

An investor is well-advised to finance more than one startup to maximize the probability of achieving at least one investment with returns that offset the inevitable capital losses on a significant portion of the portfolio. The logic of a seed or venture capital fund is to invest in a dozen promising startups, although some portfolios may include more.

To explain the performance of such a portfolio, we created a model that calculates gross exit returns based on several success scenarios for the startups it contains.

We invite you to step into the shoes of a business angel or a “small” seed fund managing €10 million to invest in 10 startups over a 10-year period. Investments are made during the first four years, and shares are held for an average of six years.

The return is expressed as a multiple of the initial investment: « X0 » means your investment results in a complete loss, while « X2 » means your investment doubles.

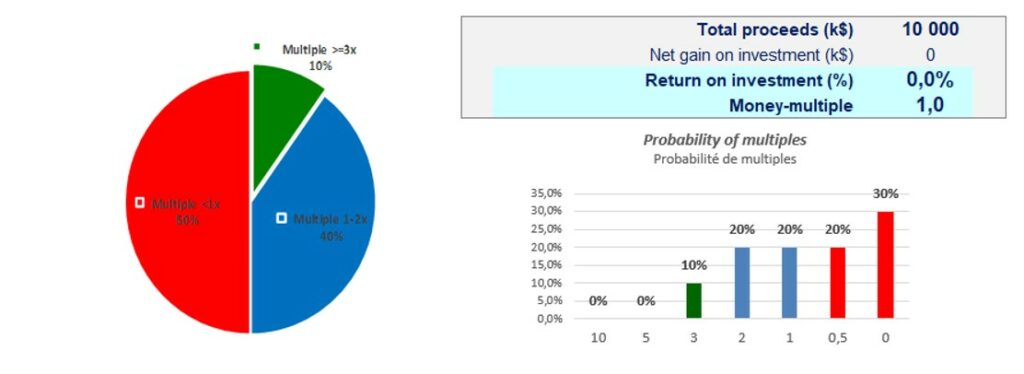

Scenario #1: Neutral Portfolio

Our first scenario is a portfolio where:

- 30% of startups, or 3 companies, result in a total loss.

- 20% of startups recover half of the initial investment.

- 20% of startups break even.

- 20% of startups double the initial investment.

- 10% of investments, or one company, yield a 3x return.

These percentages can also reflect the probability of success for a single investment.

A quick calculation shows that the total exit proceeds are €10 million, equivalent to the initial investment. Since you recover your principal without any gain or loss, this is a neutral portfolio.

We see that a single investment generating a 3x return and two investments generating a 2x return are enough to offset the weaker performances of the rest of the portfolio. This configuration corresponds to the third (penultimate) quartile of “venture and growth” funds, whose net IRR (internal rate of return) is close to zero, at +0.8%, according to the 2024 France Invest / EY study on the net performance of French private equity players.

Our neutral portfolio model, with a multiple of 1, is not far from the reality faced by many investors. As we will see in the second scenario, based on the least-performing quartile, nearly a quarter of investors recover less than half of their initial investment.

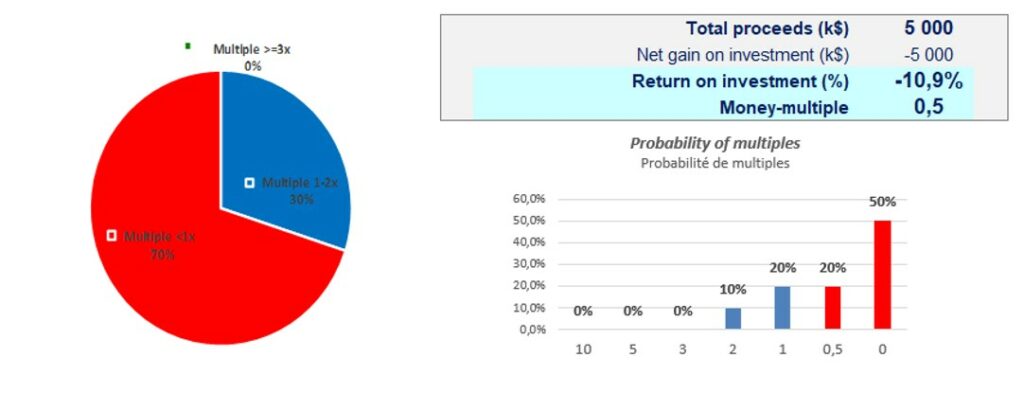

Scenario #2: Portfolio Halved

The bottom quartile in the France Invest / EY study records a return of -12.2%, which is worse than a portfolio that recovers only half the total investment. The second portfolio below shows that the €10 million invested results in €5 million. The multiple for this new scenario is 0.5, equivalent to an annual return of -10.9% over six years.

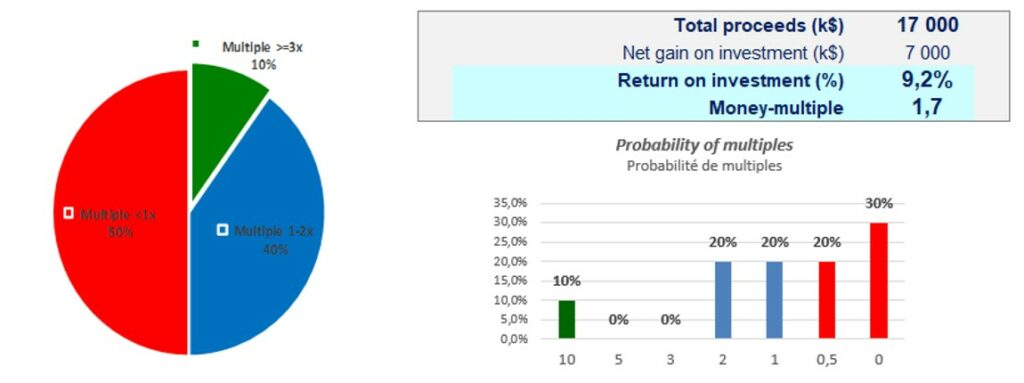

Scenario #3: Portfolio with a “Home Run” at X10

In our third portfolio, similar to Scenario #1, we replace the investment yielding a 3x return with a “home run,” i.e., an investment that alone repays the entire portfolio with a 10x multiple. The term “home run” is borrowed from baseball, referring to a play where the maximum number of points is scored through a single hit that rounds all bases.

This portfolio places us in the second quartile of the most successful investments, with an average return of +7.5%, as per the 2024 France Invest and EY study. It generates a capital gain of €7 million on the €10 million invested, resulting in a 9.2% return and a multiple of 1.7.

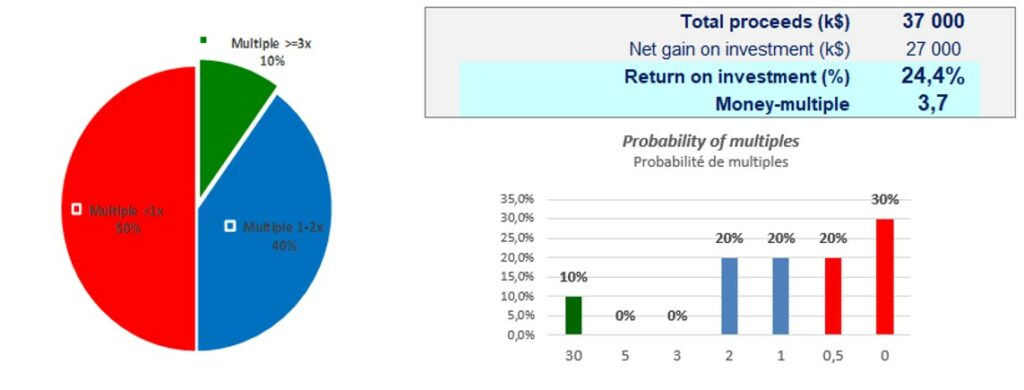

Scenario #4: “Top Quartile” Portfolio with a X30 Investment

Our fourth and final portfolio is almost identical to the previous one, except the most successful investment now generates a 30x multiple. This is similar to what early investors in Mistral AI might receive if the startup is sold for twice the valuation of its June 2024 funding round.

This new portfolio places us in the top quartile of the most successful investments, with an average return of +23.3%, as per the 2024 France Invest and EY study. It generates a capital gain of €27 million on the €10 million invested, resulting in a 24.4% return and a multiple of 3.7.

Although this model does not account for taxes, inflation, or potential management fees, this approach using multiples helps calculate the gross return of a typical portfolio.

Modern-day gold seekers must count on a “home run” within their investment portfolio. Indeed, the realization of just one extraordinary investment can place you among the coveted ranks of top-performing investors.